Management tools are a dime a dozen. And yet, contrary to popular belief, most of them are good and helpful if used correctly and in an adequately defined context.

In “Tool Box Talks” we introduce you to common and less well-known tools and show you how you can exploit their potential for your enterprise, with today’s focus on the Risk Matrix.

What is a risk matrix and when should it be used?

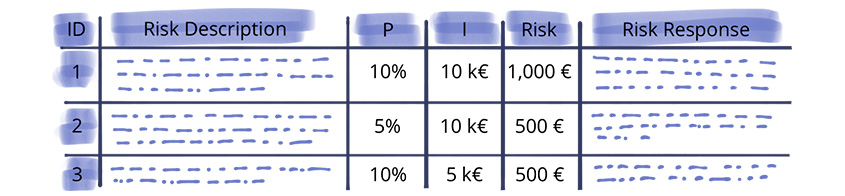

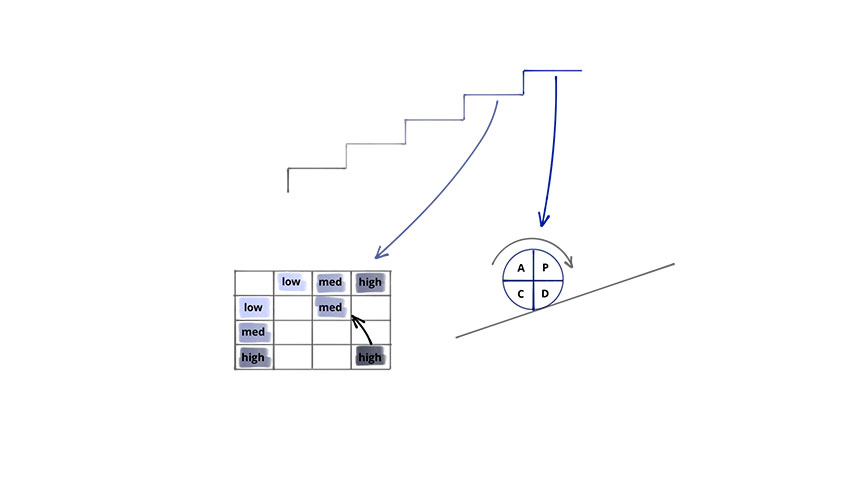

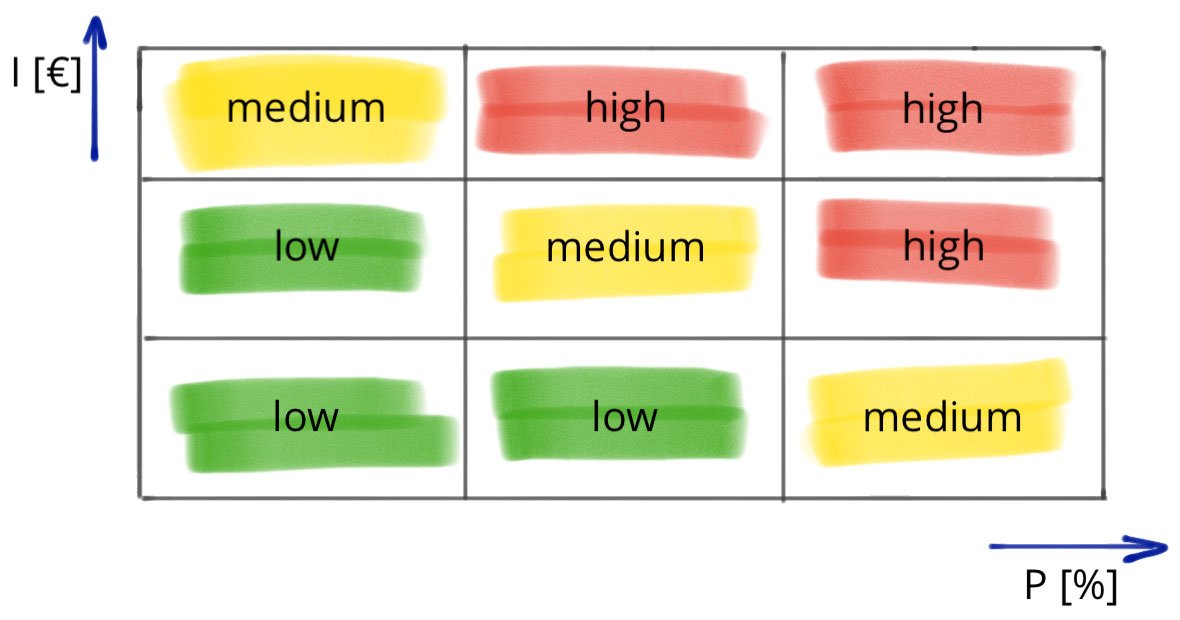

A risk matrix is a tool which helps you to deal with risks. This device visualises a risk assessment by taking account of its probability, its consequence severity and its level or priority.

To support risk managers in their work, risk matrices are often incorporated into risk registers, which they represent in a condensed and visualised form. Also, they have become customary in reporting, where they show the amount and distribution of risks in a project or in a specific operational unit

How do you use a risk matrix?

Before you can apply a risk matrix, you first have to identify and assess the risks for your project or your operational unit. Evaluating these risks works in three dimensions: probability, consequence severity and priority. The first two values can be assessed either qualitatively (high / medium / low) or quantitatively (in % or €), whereas the priority of risks is typically categorised into high / medium / low.

Depending on this assessment you then plot these risks on a two-dimensional matrix, with the x-axis representing the probability of occurrence and the y-axis corresponding to consequence severity. Priority can be visualised by the choice of different colours

Beware of pitfall

However, it is in particular due to this manner of visualising priorities that certain risks are neglected. The most frequent reaction to traffic light colours – the most often used colour for high / medium / low is red / yellow / green – is to focus on the red items by ignoring the green ones.

While it may certainly be right to prioritise some risks as ‘high’, classifying a risk as ‘low’ still does not necessarily mean that it “does not have to be dealt with actively”. So take a closer look at every single risk and double-check, no matter what the priorities, what measures you can take and which of them is suitable and should be put into action.

What is the use of a risk matrix?

A risk matrix is a tool to visualise all risks and their individual assessment. Thus it helps to quickly identify the most relevant risks – both in terms of their individual probability and consequence severity, and with regard to their priority.

This visualisation is particularly useful if you have to handle a great number of risks as it will make it easier for you to identify the most important issues at a glance and to tackle the most crucial ones first.

Furthermore, this form of graphical representation is ideal for reporting as this intelligent system of visualisation offers a valuable insight into the total number of risks and their criticality without the necessity to go through or analyse huge amounts of data.

Follow us on LinkedIn to learn on a regular basis how you can make the most of management tools, so that you will stay one step ahead of your competitors.