A serious impediment to sustainable energy supplies is its availability for customers where and when it is needed. Thus, transporting and storing energy is a crucial factor for success in the energy transition.

While electricity cannot be transmitted over longer distances without significant losses, hydrogen can be transported as well as stored without losing too much of the energy contained. But how does it work and how much will it cost customers to get their hydrogen?

In the first part of our mini-series “Hydrogen Transport: How will the customers actually get their energy?” we will answer this question on a global scale, i.e. we will analyze the international transport from the regions producing hydrogen to countries with a high demand. Regional hydrogen deployment options will be the topic of Part 2.

Rational for a global hydrogen transport

The costs of green hydrogen production are mainly determined by two factors: the cost of electricity and the availability of renewable electricity. Fasihi and Breyer as well as many other research teams have shown that some regions haver significantly better conditions for green hydrogen production than others. Among the preferred regions there are Australia, large parts of Africa and Southern America, plus some region in the US.

The demand for green hydrogen is primarily driven by the energy demand in industrial countries. According to a study by McKinsey, The offtakers will be located in the US, Europe, China, Japan and Korea. Apart from the US, all these countries are characterized by high hydrogen production costs.

Because of this discrepancy, hydrogen transport is the logical answer. But how can this be realized bearing in mind the physical properties of the substance?

Options for hydrogen transport

Being a gaseous energy carrier, the first options which come to mind are those already used for natural gas transport today, i.e. the use of pipelines and, similar to liquified natural gas (LNG), liquified hydrogen transport by ship.

The difference is the lower volumetric energy density of hydrogen. A cubic meter hydrogen only contains one third of the energy of a cubic meter natural gas – and LNG contains roughly four to five times more energy than liquified hydrogen.

To reduce volume and transportation costs, hydrogen can be converted into liquid energy carriers with higher volumetric energy density. The best known and technically most mature ones are ammonia and liquid organic hydrogen carriers (LOHC) as e.g. methanol.

What are the costs of global hydrogen transport?

The costs for transporting hydrogen by pipeline are determined by energy consumption for compression and depreciation of the piping system. According to Galimova et al., this is approximately 0.50 € per 1,000 km. Due to the strong dependency on distance, pipelines are attractive for shorter distances only, especially if new infrastructure is required which increases depreciation related costs.

For the other three options, costs are determined by three process steps: the conversion of hydrogen into the transport medium, the transport itself, and the re-conversion to hydrogen.

Liquifying hydrogen involves significant energy consumption which cannot be recovered later in the process. Besides, the transportation of liquid hydrogen requires special equipment which drives investment costs. Thus, liquid hydrogen is only feasible for shorter distances and higher volumes if no pipelines are available or new pipelines are too expensive.

Being an organic material, LOHC requires sustainable carbon which is not available in vast quantities in suitable molecules (i.e. CO or CO2). At the same time, high energy density minimizes transportation costs and, depending on the target usage, re-conversion may not be necessary as LOHC can be directly used as a source of energy. These characteristics make LOHC an attractive transport medium for longer distances but for smaller volumes and special use cases, e.g. sustainable fuels for aviation or maritime applications.

In contrast, ammonia utilizes nitrogen, which can easily be extracted from ambient air. Together with low transport costs due to a high energy density, ammonia is the preferred transport option for long distance shipping of large quantities.

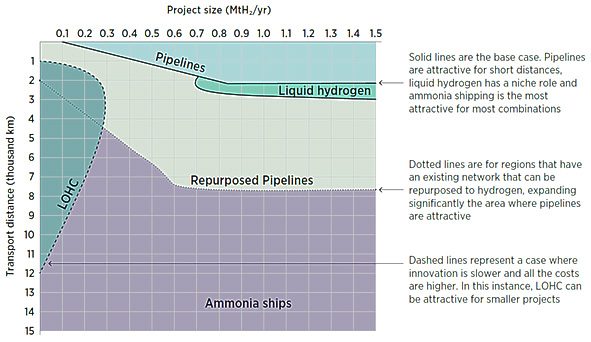

The chart above, provided by Herib Blanco, visualizes the different solutions for hydrogen transport and the related costs depending on distance and volume. According to research by Roland Berger, the expected costs range from two to five Euro per kilo of hydrogen – depending on the distance and chosen transport option